UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): May 22, 2015

Akoustis Technologies, Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 333-193467 | 33-1229046 |

| (State or Other Jurisdiction | (Commission File | (I.R.S. Employer |

| of Incorporation) | Number) | Identification Number) |

9805 Northcross Center Court, Suite H

Huntersville, NC 28078

(Address of principal executive offices, including zip code)

704-997-5735

(Registrant’s telephone number, including area code)

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

¨ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

¨ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

¨ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

¨ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

TABLE OF CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Current Report contains forward-looking statements, including, without limitation, in the sections captioned “Description of Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Plan of Operations,” and elsewhere. Any and all statements contained in this Report that are not statements of historical fact may be deemed forward-looking statements. Terms such as “may,” “might,” “would,” “should,” “could,” “project,” “estimate,” “pro-forma,” “predict,” “potential,” “strategy,” “anticipate,” “attempt,” “develop,” “plan,” “help,” “believe,” “continue,” “intend,” “expect,” “future,” and terms of similar import (including the negative of any of the foregoing) may be intended to identify forward-looking statements. However, not all forward-looking statements may contain one or more of these identifying terms. Forward-looking statements in this Report may include, without limitation, statements regarding (i) the plans and objectives of management for future operations, including plans or objectives relating to the development of commercially viable radio frequency filters, (ii) a projection of income (including income/loss), earnings (including earnings/loss) per share, capital expenditures, dividends, capital structure or other financial items, (iii) our future financial performance, including any such statement contained in a discussion and analysis of financial condition by management or in the results of operations included pursuant to the rules and regulations of the SEC, and (iv) the assumptions underlying or relating to any statement described in points (i), (ii) or (iii) above.

The forward-looking statements are not meant to predict or guarantee actual results, performance, events or circumstances and may not be realized because they are based upon our current projections, plans, objectives, beliefs, expectations, estimates and assumptions and are subject to a number of risks and uncertainties and other influences, many of which we have no control over. Actual results and the timing of certain events and circumstances may differ materially from those described by the forward-looking statements as a result of these risks and uncertainties. Factors that may influence or contribute to the inaccuracy of the forward-looking statements or cause actual results to differ materially from expected or desired results may include, without limitation, our inability to obtain adequate financing, our limited operating history, our inability to generate revenues or achieve profitability, our inability to achieve acceptance of our products in the market, upturns and downturns in the industry, our limited number of patents, failure to obtain, maintain and enforce our intellectual property rights, our inability to attract and retain qualified personnel, our substantial reliance on third parties to manufacture products, existing or increased competition, failure to innovate or adapt to new or emerging technologies, results of arbitration and litigation, stock volatility and illiquidity, and our failure to implement our business plans or strategies. A description of some of the risks and uncertainties that could cause our actual results to differ materially from those described by the forward-looking statements in this Report appears in the section captioned “Risk Factors” and elsewhere in this Report.

Readers are cautioned not to place undue reliance on forward-looking statements because of the risks and uncertainties related to them and to the risk factors. We disclaim any obligation to update the forward-looking statements contained in this Report to reflect any new information or future events or circumstances or otherwise.

Readers should read this Report in conjunction with the discussion under the caption “Risk Factors,” our financial statements and the related notes thereto in this Report, and other documents which we may file from time to time with the Securities and Exchange Commission (the “SEC”).

| 1 |

We were incorporated as Danlax, Corp., in Nevada on April 10, 2013. Prior to the Merger and Split-Off (each as defined below), our business was development and sales of mobile games.

As previously reported, on April 15, 2015, (i) we changed our name to Akoustis Technologies, Inc., and (ii) we increased our authorized capital stock from 75,000,000 shares of common stock, par value $0.001 per share, to 300,000,000 shares of common stock, par value $0.001 per share (the “Common Stock”), and 10,000,000 shares of “blank check” preferred stock, par value $$0.001 per share.

Also as previously reported, on April 23, 2015, we completed a 1.094891-for-1 forward split of our Common Stock in the form of a dividend, with the result that the 11,740,000 shares of Common Stock outstanding immediately prior to the stock split became 12,854,024 shares of Common Stock outstanding immediately thereafter. All share and per share numbers in this Report relating to our Common Stock have been adjusted to give effect to this stock spilt, unless otherwise stated.

On May 22, 2015, our wholly owned subsidiary, Akoustis Acquisition Corp., a corporation formed in the State of Delaware on May 15, 2015 (“Acquisition Sub”) merged (the “Merger”) with and into Akoustis, Inc., a corporation incorporated in the State of Delaware on May 12, 2014. Akoustis, Inc., was the surviving corporation in the Merger and became our wholly owned subsidiary. All of the outstanding stock of Akoustis, Inc., was converted into shares of our Common Stock, as described in more detail below.

In connection with the Merger and pursuant to the Split-Off Agreement (defined below), we transferred our pre-Merger assets and liabilities to our pre-Merger majority stockholder, in exchange for the surrender by him and cancellation of 9,854,019 shares of our Common Stock. See Item 2.01, “Split-Off,” below.

As a result of the Merger and Split-Off, we discontinued our pre-Merger business and acquired the business of Akoustis, Inc., and will continue the existing business operations of Akoustis, Inc., as a publicly-traded company under the name Akoustis Technologies, Inc.

Also on May 22, 2015, we closed a private placement offering (the “Offering”) of 3,531,104 shares of our Common Stock, at a purchase price of $1.50 per share. Additional information concerning the Offering is presented below under Item 2.01, “Merger and Related Transactions—the Offering” and “Description of Securities,” and Item 3.02, “Unregistered Sales of Equity Securities.”

In accordance with “reverse merger” accounting treatment, our historical financial statements as of period ends, and for periods ended, prior to the Merger will be replaced with the historical financial statements of Akoustis, Inc., prior to the Merger in all future filings with the SEC.

Also on May 22, 2015, we changed our fiscal year from a fiscal year ending on July 31 of each year, which was used in our most recent filing with the SEC, to one ending on March 31 of each year, which is the fiscal year end of Akoustis, Inc.

As used in this Current Report henceforward, unless otherwise stated or the context clearly indicates otherwise, the terms “Akoustis,” the “Company,” the “Registrant,” “we,” “us,” and “our” refer to Akoustis Technologies, Inc., incorporated in Nevada, after giving effect to the Merger and the Split-Off.

This Current Report contains summaries of the material terms of various agreements executed in connection with the transactions described herein. The summaries of these agreements are subject to, and are qualified in their entirety by, reference to these agreements, which are filed as exhibits hereto and incorporated herein by reference.

| 2 |

This Current Report is being filed in connection with a series of transactions consummated by the Company and certain related events and actions taken by the Company.

This Current Report responds to the following Items in Form 8-K:

| Item 1.01. | Entry into a Material Definitive Agreement |

| Item 2.01. | Completion of Acquisition or Disposition of Assets |

| Item 3.02. | Unregistered Sales of Equity Securities |

| Item 4.01. | Changes in Registrant’s Certifying Accountant |

| Item 5.01. | Changes in Control of Registrant |

| Item 5.02. | Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers |

| Item 5.06. | Change in Shell Company Status |

| Item 9.01. | Financial Statements and Exhibits |

Prior to the Merger, we were a “shell company” (as such term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). As a result of the Merger, we have ceased to be a shell company. The information contained in this Current Report, together with the information contained in our Annual Report on Form 10-K for the fiscal year ended July 31, 2014, and our subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, as filed with the SEC, constitute the current “Form 10 information” necessary to satisfy the conditions contained in Rule 144(i)(2) under the Securities Act of 1933, as amended (the “Securities Act”).

| 3 |

| ITEM 1.01 | ENTRY INTO A MATERIAL DEFINITIVE AGREEMENT |

The information contained in Item 2.01 below relating to the various agreements described therein is incorporated herein by reference.

| ITEM 2.01 | COMPLETION OF ACQUISITION OR DISPOSITION OF ASSETS |

The Merger and Related Transactions

Merger Agreement

On May 22, 2015 (the “Closing Date”), the Company, Acquisition Sub and Akoustis, Inc., entered into an Agreement and Plan of Merger and Reorganization (the “Merger Agreement”), which closed on the same date. Pursuant to the terms of the Merger Agreement, Acquisition Sub merged with and into Akoustis, Inc., which was the surviving corporation and thus became our wholly-owned subsidiary.

Pursuant to the Merger, we acquired the business of Akoustis, Inc., of developing advanced, more efficient bulk acoustic wave filters for use in mobile and wearable devices.

At the closing of the Merger each of the 11,671 shares of common stock and the 5,300 shares of preferred stock of Akoustis, Inc., issued and outstanding immediately prior to the closing of the Merger was converted into 324.082 shares of our Common Stock. As a result, an aggregate of 5,500,006 shares of our Common Stock were issued to the holders of Akoustis, Inc., stock.

The Merger Agreement contained customary representations and warranties and pre- and post-closing covenants of each party and customary closing conditions. Breaches of the representations and warranties will be subject to indemnification provisions. Each of the stockholders of Akoustis, Inc., as of the date of the Merger initially received in the Merger 95% of the shares to which each such stockholder is entitled, with the remaining 5% of such shares being held in escrow for two (2) years to satisfy post-closing claims for indemnification by the Company (“Indemnity Shares”). Any of the Indemnity Shares remaining in escrow at the end of such two-year period shall be distributed to the pre-Merger stockholders of Akoustis, Inc., on a pro rata basis. The Merger Agreement also contains a provision providing for a post-Merger share adjustment as a means for which claims for indemnity may be made by the pre-Merger stockholders of Akoustis, Inc. Pursuant to this provision up to 250,000 additional shares (“R&W Shares”) of Common Stock may be issued to the pre-Merger stockholders of Akoustis, Inc., pro rata, during the two-year period following the Merger for breaches of representations and warranties by the Company. The value of the Indemnity Shares and the R&W Shares issued pursuant to the foregoing adjustment mechanisms is fixed at the per share of Common Stock equivalent price of the securities sold in the Offering. The foregoing mechanisms are the exclusive remedies of the Company on the one hand and the pre-Merger stockholders of Akoustis, Inc., on the other hand for satisfying indemnification claims under the Merger Agreement.

The Merger will be treated as a recapitalization of the Company for financial accounting purposes. Akoustis, Inc. will be considered the acquirer for accounting purposes, and our historical financial statements before the Merger will be replaced with the historical financial statements of Akoustis, Inc., before the Merger in all future filings with the SEC.

The Merger is intended to be treated as a tax-free reorganization under Section 368(a) of the Internal Revenue Code of 1986, as amended.

The issuance of shares of our Common Stock to holders of Akoustis, Inc., capital stock in connection with the Merger was not registered under the Securities Act, in reliance upon the exemption from registration provided by Section 4(a)(2) of the Securities Act, which exempts transactions by an issuer not involving any public offering, and Regulation D promulgated by the SEC under that section. These securities may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirement, and are subject to further contractual restrictions on transfer as described below.

| 4 |

We also agreed not to register under the Securities Act the resale of the shares of our Common Stock received in the Merger by stockholders of Akoustis, Inc., for a period of two years following the closing of the Merger.

The form of the Merger Agreement is filed as an exhibit to this Report. All descriptions of the Merger Agreement herein are qualified in their entirety by reference to the text thereof filed as an exhibit hereto, which is incorporated herein by reference.

Split-Off

Upon the closing of the Merger, under the terms of a split-off agreement and a general release agreement, the Company transferred all of its pre-Merger operating assets and liabilities to its wholly-owned special-purpose subsidiary, Danlax Enterprise Corp., a Nevada corporation (“Split-Off Subsidiary”), formed on May 15, 2015. Thereafter, pursuant to the split-off agreement, the Company transferred all of the outstanding shares of capital stock of Split-Off Subsidiary to Ivan Krikun, the pre-Merger majority stockholder of the Company, and the former sole officer and director of the Company (the “Split-Off”), in consideration of and in exchange for (i) the surrender and cancellation of an aggregate of 9,854,019 shares of our Common Stock held by Mr. Krikun (which were cancelled and will resume the status of authorized but unissued shares of our Common Stock) and (ii) certain representations, covenants and indemnities. All descriptions of the split-off agreement and the general release agreement herein are qualified in their entirety by reference to the text thereof filed as exhibits hereto, which are incorporated herein by reference.

The Offering

Concurrently with the closing of the Merger and in contemplation of the Merger, we held a closing of our Offering in which we sold 3,531,104 shares of our Common Stock (including shares issued on conversion of convertible notes of Akoustis, Inc., as described below), at a purchase price of $1.50 per share (the “Offering Price”).

Investors in the shares will have anti-dilution protection with respect to the shares of Common Stock sold in the Offering such that if within 12 months after the final closing of the Offering the Company shall issue additional shares of Common Stock or Common Stock equivalents (subject to customary exceptions, including but not limited to issuances of awards under the Company’s 2015 Plan (as defined below) and certain issuances of securities in connection with credit arrangements, equipment financings, lease arrangements or similar transactions) for a consideration per share less than the Offering Price (the “Lower Price”), each such investor will be entitled to receive from the Company additional shares of Common Stock in an amount such that, when added to the number of shares of Common Stock initially purchased by such investor, will equal the number of shares of Common Stock that such investor’s Offering subscription amount would have purchased at the Lower Price.

The aggregate gross proceeds from the Offering were $5,296,656 (including $645,000 principal amount of convertible notes of Akoustis, Inc., that converted into our Common Stock by their terms upon closing of the Offering, at a conversion price per share equal to the Offering Price, and before deducting placement agent fees and expenses of the offering estimated at approximately $763,000).

The Offering was exempt from registration under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemption provided by Regulation D promulgated by the SEC thereunder. The Common Stock in the Offering was sold to “accredited investors,” as defined in Regulation D, and was conducted on a “best efforts” basis.

| 5 |

The closing of the Offering and the closing of the Merger were conditioned upon each other.

In connection with the Offering, we agreed to pay Northland Securities, Inc., and Katalyst Securities LLC, each a U.S. registered broker-dealer (the “Placement Agents”) a cash commission of 10% of the gross proceeds (or 2% in the case of certain existing Akoustis, Inc., investors) raised from investors in the Offering. In addition, the Placement Agents received warrants to purchase a number of shares of Common Stock equal to 10% (or 2% in the case of certain existing Akoustis, Inc., investors) of the number of shares of Common Stock sold in the Offering, with a term of five (5) years and an exercise price of $1.50 per share (the “Placement Agent Warrants”). Any sub-agent of the Placement Agents that introduced investors to the Offering was entitled to share in the cash fees and warrants attributable to those investors as described above.

As a result of the foregoing, the Placement Agents and their sub-agents were paid an aggregate commission of $470,266 and were issued Placement Agent Warrants to purchase an aggregate of 313,510 shares of our Common Stock. We were also required to reimburse the Placement Agents approximately $77,150 of legal expenses incurred in connection with the Offering.

We agreed to indemnify the Placement Agents and their sub-agents to the fullest extent permitted by law, against certain liabilities that may be incurred in connection with the Offering, including certain civil liabilities under the Securities Act, and, where such indemnification is not available, to contribute to the payments the Placement Agents and their sub-agents may be required to make in respect of such liabilities.

All descriptions of the Placement Agent Warrants herein are qualified in their entirety by reference to the text thereof filed as exhibits hereto, which are incorporated herein by reference.

Registration Rights

In connection with the Offering, we entered into a Registration Rights Agreement, pursuant to which we have agreed that promptly, but no later than 90 calendar days from the final closing of the Offering, the Company will file a registration statement with the SEC (the “Registration Statement”) covering (a) the shares of Common Stock issued in the Offering, (b) the shares of Common Stock issuable upon exercise of the Placement Agent Warrants, (c) any shares of Common Stock issuable to investors in the Offering pursuant to the anti-dilution rights described above and (d) 1,841,606 additional shares of Common Stock held by a pre-Merger stockholder (the “Registrable Shares”). The Company shall use its commercially reasonable efforts to ensure that such Registration Statement is declared effective within 180 calendar days after filing with the SEC. If the Company is late in filing the Registration Statement or if the Registration Statement is not declared effective within 180 days after filing with the SEC, the Company will make payments to each holder of Registrable Securities as liquidated damages at a rate equal to 12% of the Offering Price per annum for each share affected during the period that (i) the Company is late in filing the Registration Statement or (ii) the Registration Statement is late in being declared effective by the SEC; provided, however, that in no event shall the aggregate of any such liquidated damages exceed 8% of the Offering Price per share. No liquidated damages shall accrue with respect to any Registrable Shares removed from the Registration Statement in response to a comment from the staff of the SEC limiting the number of shares of Common Stock which may be included in the Registration Statement (a “Cutback Comment”) or after the shares may be resold under Rule 144 under the Securities Act or another exemption from registration under the Securities Act.

| 6 |

The Company must keep the Registration Statement “evergreen” for two (2) years from the date it is declared effective by the SEC or until Rule 144 is available to the holders of Registrable Shares who are not and have not been affiliates of the Company with respect to all of their Registrable Shares, whichever is earlier.

The holders of Registrable Shares (including any shares of Common Stock removed from the Registration Statement as a result of a Cutback Comment) and the stockholders of the Company prior to the Merger (but not holders of the shares issued to the stockholders of Akoustis, Inc., in consideration for the Merger) shall have “piggyback” registration rights for such Registrable Shares with respect to any registration statement filed by the Company following the effectiveness of the Registration Statement that would permit the inclusion of such shares, subject to customary cutback pro rata in an underwritten offering.

We will pay all expenses in connection with any registration obligation provided in the registration Rights Agreement, including, without limitation, all registration, filing, stock exchange fees, printing expenses, all fees and expenses of complying with applicable securities laws, and the fees and disbursements of our counsel and of our independent accountants. Each investor will be responsible for its own sales commissions, if any, transfer taxes and the expenses of any attorney or other advisor such investor decides to employ.

All descriptions of the Registration Rights Agreement herein are qualified in their entirety by reference to the text thereof filed as an exhibit hereto, which is incorporated herein by reference.

2015 Equity Incentive Plan

Before the Merger, our Board of Directors adopted, and our stockholders approved, the 2015 Equity Incentive Plan (the “2015 Plan”), which provides for the issuance of incentive awards of up to 1,200,000 shares of our Common Stock to officers, employees, consultants and directors. See “Market Price of and Dividends on Common Equity and Related Stockholder Matters—Securities Authorized for Issuance under Equity Compensation Plans” below for more information about the 2015 Plan and outstanding stock options.

Departure and Appointment of Directors and Officers

Our Board of Directors is authorized to consist of, and currently consists of, five members. On the Closing Date, Ivan Krikun, our sole director before the Merger, resigned his position as a director, and Jeffrey Shealy, Steve Denbaars, Jerry Neal, Arthur Geiss and Jeffrey McMahon were appointed to the Board of Directors.

Also on the Closing Date, Mr. Krikun, our Chief Executive Officer, President, Secretary and Treasurer before the Merger, resigned from these positions, and our Board of Directors appointed Jeffrey Shealy as our Chief Executive Officer, President and Chairman of the Board of Directors, Cindy Payne as our Chief Financial Officer, David Aichele as our Vice President of Business Development, Mark Boomgarden as our Vice President of Operations.

See “Management – Directors and Executive Officers” below for information about our new directors and executive officers.

Lock-up Agreements and Other Restrictions

In connection with the Merger, each of our executive officers and directors named above and each of the stockholders of Akoustis, Inc., who received shares of our Common Stock in the Merger (each a “Restricted Holder”, and, collectively, the “Restricted Holders”), holding at that date in the aggregate 5,734,006 shares of our Common Stock, entered into agreements (the “Lock-Up Agreements”), whereby they are restricted for a period of 24 months after the Merger from certain sales or dispositions of our Common Stock held by them immediately after the Merger, except in certain limited circumstances (the “Lock-Up”).

| 7 |

In addition, each Restricted Holder has agreed in the Lock-Up Agreement that it will not, for a period of 24 months following the Closing Date, directly or indirectly, effect or agree to effect any short sale (as defined in Rule 200 under Regulation SHO of the Exchange Act), whether or not against the box, establish any “put equivalent position” (as defined in Rule 16a-1(h) under the Exchange Act) with respect to the Common Stock, borrow or pre-borrow any shares of Common Stock, or grant any other right (including, without limitation, any put or call option) with respect to the Common Stock or with respect to any security that includes, relates to or derives any significant part of its value from the Common Stock or otherwise seek to hedge its position in the Common Stock.

Pro Forma Ownership

Immediately after giving effect to (i) the Merger and (ii) the cancellation of 9,854,019 shares in the Split-Off, and (iii) the closing of the Offering, there were 12,131,115 issued and outstanding shares of our Common Stock, as follows:

| · | The stockholders of Akoustis, Inc., prior to the Merger hold 5,500,006 shares of our Common Stock; |

| · | the stockholders of the Company prior to the Merger hold 3,000,005 shares of our Common Stock; |

| · | a consultant holds 100,000 shares of our Common Stock; and |

| · | investors in the Offering hold 3,531,104 shares of our Common Stock. |

In addition,

| · | the Placement Agents and their sub-agents hold Placement Agent Warrants to purchase 313,510 shares of our Common Stock; and |

| · | the 2015 Plan authorizes issuance of up to 1,200,000 shares of our Common Stock as incentive awards to executive officers, key employees, consultants and directors; options to purchase 160,000 shares of our Common Stock have been granted under the 2015 Plan to date. |

See “Description of Securities” below. No other securities convertible into or exercisable or exchangeable for our Common Stock are outstanding.

Our common stock is quoted on the OTC Markets (OTCQB) under the symbol “AKTS,” which changed from “DNLX” on May 1, 2015.

| 8 |

Accounting Treatment; Change of Control

The Merger is being accounted for as a “reverse merger,” and Akoustis, Inc., is deemed to be the accounting acquirer in the reverse merger for accounting purposes. Consequently, the assets and liabilities and the historical operations that will be reflected in the financial statements prior to the Merger will be those of Akoustis, Inc., and will be recorded at the historical cost basis of Akoustis, Inc., and the consolidated financial statements after completion of the Merger will include the assets and liabilities of Akoustis, Inc., historical operations of Akoustis, Inc., and operations of the Company and its subsidiaries from the closing date of the Merger. As a result of the issuance of the shares of our Common Stock pursuant to the Merger, a change in control of the Company occurred as of the date of consummation of the Merger. Except as described in this Current Report, no arrangements or understandings exist among present or former controlling stockholders with respect to the election of members of our Board of Directors and, to our knowledge, no other arrangements exist that might result in a change of control of the Company.

We continue to be a “smaller reporting company,” as defined under the Exchange Act, following the Merger. We believe that as a result of the Merger we have ceased to be a “shell company” (as such term is defined in Rule 12b-2 under the Exchange Act).

Immediately following the Merger, the business of Akoustis became our business.

Corporate Information

As described above, we were incorporated in Nevada as Danlax, Corp. on April 10, 2013. Our original business was development and sale of mobile games. Prior to the Merger, our Board determined to discontinue operations in this area and to seek a new business opportunity. As a result of the Merger, we have acquired the business of Akoustis.

Akoustis was incorporated on May 12, 2014, under the laws of the State of Delaware and commenced doing business in North Carolina in May 2014.

Our authorized capital stock currently consists of 300,000,000 shares of the Common Stock, and 10,000,000 shares of the Preferred Stock. Our Common Stock is quoted on the OTC Markets (OTCQB) under the symbol “AKTS,” which changed from “DNLX” on May 1, 2015.

Our principal executive offices are located at 9805 Northcross Center Court, Suite H, Huntersville, NC 28078. Our federal Employer Identification Number (EIN) is 33-1229046; the EIN of Akoustis, Inc., is 46-5645617. Our telephone number is 704-997-5735. Our website address is www.akoustis.com. (The information contained on, or that can be accessed through, our website is not a part of this Report.)

“Akoustis™,” the Akoustis logo and “Bulk ONE™” are our trademarks. This Report may contain additional trade names, trademarks and/or service marks of other companies. We do not intend our use or display of other companies’ trade names, trademarks, or service marks to imply a relationship with these other companies, or endorsement or sponsorship of us by these other companies. Other trademarks appearing in this prospectus are the property of their respective holders.

| 9 |

Glossary

The following is a glossary of technical terms used herein:

| • | Acoustic wave—a mechanical wave that vibrates in the same direction as its direction of travel. |

| • | Acoustic wave filter—a electromechanical device that provides radio frequency control and selection, in which an electrical signal is converted into a mechanical wave in a device constructed of a piezoelectric material and then back to an electrical signal. |

| • | Band, channel or frequency band—a designated range of radio wave frequencies used to communicate with a mobile device. |

| • | Bulk acoustic wave (BAW)—an acoustic wave traveling through a material exhibiting elasticity, typically vertical or perpendicular to the surface of a piezoelectric material. |

| • | Digital baseband—the digital transceiver, which includes the main processor for the communication device. |

| • | Duplexer—a bi-directional device that connects the antenna to the transmitter and receiver of a wireless device and simultaneously filters both the transmit signal and receive signal. |

| • | Filter—a series of interconnected resonators designed to pass (or select) a desired radio frequency signal and block unwanted signals. |

| • | Group III element nitrides—single crystal nitride crystal containing at least one element from the Group III metals in the period table (scandium (Sc), yttrium (Y), lanthanum (La) and actinium (Ac)). |

| • | Monolithic topology—a description of an electrical circuit whereby all the elements of the circuit are fabricated at the same time using the same process flow. |

| • | Power Amplifier Duplexer (PAD)—an RF module containing a power amplifier and duplex filter components for the RF front-end of a smartphone. |

| • | Piezoelectric materials—certain solid materials (such as crystals and certain ceramics) that produce a voltage in response to applied mechanical stress, or that deform when a voltage is applied to them. |

| • | Resonator—a device whose impedance sharply changes over a narrow frequency range and is characterized by one or more ‘resonance frequency’ due to a standing wave across the resonator’s electrodes. The vibrations in a resonator can be either electromagnetic or mechanical (including acoustic). Resonators are the building blocks for RF filters used in mobile wireless devices. |

| • | RF—radio frequency |

| • | RF front-end—the circuitries in a mobile device responsible for processing the analog radio signals and is located between the device’s antenna and the digital baseband. |

| • | Surface acoustic wave (SAW)—an acoustic wave traveling horizontally along the surface of a material. |

| 10 |

Overview

Akoustis™ is an early stage, “fabless” company developing, designing and manufacturing innovative filter products for radio frequency, or RF, front-ends for the mobile wireless device industry. We use a fundamentally new piezoelectric resonator technology that we call Bulk ONE™ in the manufacturing of acoustic resonators, the building blocks of high selectivity “RF” filters required to route signals in a smartphone or other mobile or wearable device. Filters are a critical component of the RF front-end, and their use has multiplied with the launch and licensing of 4G/LTE frequency bands. They are used to define the range of frequencies of radio signals that are transmitted (the “passband”) and simultaneously reject unwanted signals. The increasing demand for wireless data and user applications is driving an increase in the number of wireless channels or frequency bands in a single device. Each new band introduced creates an increase in a demand for filters. A high-end smartphone, for example, must filter the transmit and receive paths for 2G, 3G and 4G wireless access methods in up to 15 bands, as well as Wi-Fi, Bluetooth and in some cases GPS. Signals in the receive paths must be isolated from one another. The filters also must reject other extraneous signals from numerous sources. The current approach to RF filter manufacturing utilizes thin-film polycrystalline materials (thin-film bulk acoustic resonators, or “FBARs”) with relatively high resistance that dissipate a significant amount of the energy in the signal (referred to as “lossy”), resulting in front-end heat generation and reduced battery life. In order to compensate for such losses, the power amplifier specifications are increased, by as much as a factor of two, which reduces further the battery life and puts more demands on the thermal management of the mobile device.

As the filter count per mobile device increases, these inefficiencies will become more limiting. We plan to use single crystal piezoelectric materials to develop a new class of filters with a fundamental advantage to reduce losses over existing thin film technologies. We have fabricated R&D resonators demonstrating the feasibility of our Bulk ONE technology, and are in the process of transitioning the technology into a production-capable wafer fabrication facility for the ultimate purpose of manufacturing our bulk mode acoustic wave filters. Our business model involves “fabless” manufacturing, meaning that we leverage capital investments and capacity of our strategic partners to manufacture our wafers. Once our technology is qualified for manufacturing, we expect to design and sell single crystal filter products using our Bulk ONE technology.

We believe our technology is disruptive to the RF front-end market through the following expected advantages:

| • | Lower insertion loss, |

| • | Wider bandwidth coverage, |

| • | Improved power compression and linearity, |

| • | Reduced power amplifier cost, |

| • | Reduced heat generation and reduced battery loading, and |

| • | Reduced guard band between adjacent frequency bands. |

Once our Bulk ONE technology is qualified for production, our product focus is on innovative single-band filter products for the growing RF front-end market, which can be used to make duplexer or multiplexer filter products necessary for the Mobile Internet. These products present the greatest near-term potential for commercialization of our technology. According to a McKinsey Global Institute report, the Mobile Internet and the so-called “Internet of Things” (IoT) is one of the twelve potentially economically disruptive technologies with an estimated economic value impact that could be over $25 trillion.

| 11 |

Our Technology

Current RF filters utilize a technology that is limited by the material properties of the base filter component. Existing bulk acoustic wave filters use an “acoustic wave ladder” that is based on a monolithic topology approach using lossy polycrystalline materials. By contrast, our Bulk ONE technology uses a single crystal material, which provides 30% higher piezoelectric properties, compared to conventional polycrystalline materials used in the industry today. We have fabricated R&D resonators that demonstrate the feasibility of our approach and believe our technology will yield a new generation of filter products.

Bulk ONE Technology consists of novel single-crystal piezoelectric materials, which are fabricated into bulk-mode, acoustic wave resonators and RF filters. Our patent-pending piezoelectric materials contain high-purity Group III element nitride materials and possess a unique signature, which can be detected by conventional material metrology tools. We utilize analytical modeling techniques to aid in the design of our materials and our material specifications are typically outsourced to a third party for manufacturing. Once our materials are ready for processing, we supply our wafer manufacturing partner raw materials, a mask design file, and unique process flow in order to fabricate our resonators and filters. Our wafer process flow contains a process module for wafer level packaging (WLP) that allows for low profile, cost effective filters to be produced.

Challenges Faced by the Mobile Device Industry

Rising consumer demand for always-on wireless broadband connectivity is creating an unprecedented need for high performance RF Front End for mobile devices. Mobile devices such as smartphones and tablets are quickly driving the Internet of Things (IoT). The rapid growth in mobile data traffic is testing the limits of existing wireless bandwidth. Carriers and regulators have responded by opening new swaths of RF spectrum, driving up the number of frequency bands in mobile devices. This substantial increase in frequency bands has created a demand for more filters, as well as a demand for filters with higher selectivity. The global transition to LTE and adoption of LTE-Advanced with more sophisticated carrier aggregation and multiple-input, multiple-output (MIMO) techniques will continue to push the requirements for increased supply of high performance filters.

Furthermore, the new spectrum introduced by 4G/LTE is driving licensing at higher frequencies than previous 3G smartphone models. For example, new TDD LTE frequencies allocated for 4G wireless cover frequencies nearly twice has high as covered in previous generation phones. As a result, the demand for high frequency or “high band” filters has exploded according a Mobile Experts 2014 report. For traditional “low band” frequencies, SAW filters have been the primary choice, while high band solutions have utilized BAW filters due to their performance and yield. While there are multiple sources of supply for SAW technology, the source of supply for BAW filters is more limited and essentially dominated by two manufacturers worldwide.

The first problem is that signal loss of current generation acoustic wave filters is excessively high, and up to half of the transmit power is wasted as heat, which ultimately constrains battery life. In addition, filters with inferior selectivity either reduce the available operating bands the mobile device can support or increase the noise in the operating bands. Each of these problems negatively impacts the end-user’s experience when using the mobile device.

| 12 |

Our Solutions

Our immediate focus is on the commercialization of filters using our Bulk ONE technology. We believe these filters enable new PAD module or RF Front-end competition for high band modules as well as performance-driven low band applications. Initially, we expect to target select strategic market leaders as well as Tier 2 mobile wireless module suppliers. Longer term, our focus will be to expand our market share by engaging with multiple module manufacturers. We are currently partnering with a wafer manufacturer to commercialize our first filters using our Bulk ONE technology. This will be the first in a series of R&D activities that will set the foundation for filter products that we believe can disrupt the high band filter market. We will develop a series of filter designs used in the manufacturing of duplexers or more complex multiplexers targeting the 4G/LTE frequency bands. We believe our filter designs will create an alternative and replace filters currently manufactured using materials with fundamentally inferior performance.

Our Business Model

We will provide filters to the market through the manufacturing of our product using a “fabless” outsourced manufacturing model. By leveraging the existing manufacturing capacity of our partner, we will operate a capital-efficient business. Our target customers will be those companies that make part of or the entire RF front-end module. We expect sales of our filters to RF front-end module manufacturers will be the source of our revenue. We will principally provide design and development resources and manage our outsourced partners to support our product realization process. There are two companies specializing in manufacturing of BAW filters that dominate this market. See “Competition” below. We believe our Bulk ONE technology provides a competitive filter alternative and that there will be factors creating significant barriers to entry for potential additional competitors:

| • | Our growing portfolio of intellectual property (see “Intellectual Property” below); |

| • | Our highly experienced leadership and technical team; and |

| • | Being first to market with a competitive filter alternative. |

Our History

Akoustis was founded in 2014 by experienced industry leaders and scientists from University of California at Santa Barbara (UCSB) and Cornell University. Our initial funding was through a $0.5 million series seed funding in 2014, and we received $655,000 in additional investments in convertible notes and stock by the founders and original angel investors in March and April 2015. We received a National Science Foundation (“NSF”) Small Business Innovation Research (“SBIR”) grant that started in January 2015. In addition, we received matching funds from North Carolina Science, Technology & Innovation Department of Commerce. The funds from these sources have supported the operations of Akoustis. Akoustis has used these funds to finance the completion of multiple key milestones. These milestones include the application for seven patents with over 200 claims, hiring of key personnel, the engagement with a foundry prototype facility for the development of a single crystal resonator demonstrator, initiation of SBIR activities that include modeling to design evaluation deliverables, and the engagement and securing of strategic partners for the supply and fabrication of the filters using our Bulk ONE technology.

| 13 |

The Mobile Internet

Rising consumer demand for always-on wireless broadband connectivity is creating an unprecedented need for high performance RF front-ends for mobile devices. Mobile devices such as smartphones and tablets are quickly becoming the primary means of accessing the Internet. The exponential growth in mobile data traffic is testing the limits of existing wireless bandwidth. Carriers and regulators have responded by opening new RF spectrum, driving up the number of frequency bands in mobile devices. As a prime example, a Presidential directive was issued in 2010 to the FCC and other agencies to make available an additional 500 MHz of RF spectrum to meet the growing demand in the United States. Similar initiatives are occurring worldwide. Adding RF spectrum is not a complete solution. The added spectrum does not come in large contiguous blocks, but rather in small channels or bands of varying size and frequency. Thus, more data means more bands, and the result is a rapid and substantial increase in the number of filters in mobile devices.

The Challenge

Moore’s Law predicts that transistor density on integrated circuits will double approximately every two years, and the digital baseband of mobile devices has improved exponentially as predicted by Moore’s Law. However, improvements to the analog RF front-end have been limited by existing filter technology, with only incremental updates to existing technology. Consequently, the RF front-end is taking up an ever-growing share of the total cost of mobile devices. Most mobile devices sold today operate on “fourth generation” wireless technology, or 4G. There are nearly fifty 4G bands recognized worldwide today, and the list is growing. The RF front-end must meet these growing data demands while reducing cost and improving battery life. Our solution involves a new approach to RF component manufacturing, enabled by Bulk ONE technology. Our technology will produce filters that will reduce the overall system cost and improve performance of the RF front-end.

Figure 1—Our Solution

| 14 |

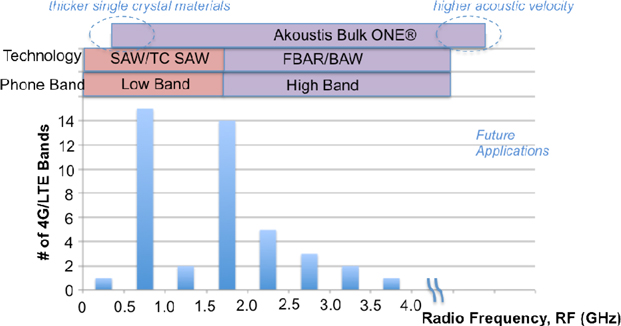

Single-Band Designs for Duplexers and Multiplexers

SAW filters have been preferred in modern RF front-ends because of their high performance, small size and low cost. However, traditional SAW ladder designs do not perform well in high frequency bands or bands with closely spaced receive and transmit channels, typical of many new bands. Therefore, larger BAW filters are needed for these bands. We have demonstrated in a development environment our ability to fabricate BAW resonators, the building block of BAW filters, that are more efficient than existing available BAW resonators, and we believe the improved efficiency will reduce the total cost of RF front-ends as well as reduce the battery demand for mobile devices. Additionally, we believe that our Bulk ONE filters will allow for a single manufacturing method that will support all of the BAW filter band range and a significant portion of the SAW band range. Figure 2 below illustrates what we believe will be the frequency range of our Bulk ONE technology.

Figure 2— The potential range of our technology

Pure-Play Filter Provider Enables New Module Competition

Our technology allows for a wide range of frequency coverage, and we plan to supply filters that will support 4G/LTE and beyond. We have successfully demonstrated resonators that will support the design and fabrication of 4G/LTE filters, and our current focus is on completing the development required to transition this single-crystal BAW technology to high volume manufacturing. We will be a pure-play filter supplier that will address the increasing RF complexity placed on RF front-end manufacturers supporting 4G/LTE.

| 15 |

Figure 3— Projected Growth (Source: Ericsson)

Commercialization

Our immediate focus is to address problems in the RF front-end with innovative single-band designs using our Bulk ONE technology. We are currently developing our first commercial single-band filter in collaboration with a manufacturing partner, Global Communication Semiconductors, LLC (“GCS”), under the terms of a signed development agreement. Both parties are focused on developing fixed-band filters because we believe these designs present the greatest near-term potential for commercialization of our technology, and that once demonstrated, there is a shorter learning curve for having the foundry ready for production.

The development agreement with GCS contains the following milestones:

| • | Milestone 1 (Manufacturing Partner Gap Analysis)—Validate required materials, people, process and equipment are present for volume manufacturing. |

| • | Milestone 2 (Process Transfer to Foundry Partner)—Design of filters, technology transfer and fabrication on GCS’s high-volume manufacturing equipment, fully tested wafers, and delivery of prototypes. |

| • | Milestone 3 (Complete Filter Process Capability)—Update design with process feedback, fabricate multiple wafers using the approved manufacturing process flow, fully tested wafers, calculated yield and delivery of initial product. |

| • | Milestone 4 (Production-Ready Filter Design)—Filter design complete, manufacturing process locked, product fully packaged and ready for production, focus shift to revenue generation from filter sales. |

Milestone 1 is complete. Management expects to complete work on Milestone 2 before the end of June 2016, at which time we plan to commence work on Milestone 3, with an expected completion by September 2016. We expect to generate revenue from the sale of our filters in early 2017 after completion of Milestone 4, which we currently target by end of 2016.

| 16 |

Research and Development

Since inception, the Company’s focus has been on developing an innovative mobile-wireless filter technology with a compelling value proposition to our potential customers and a significant and noticeable impact to the end user.

Whereas today’s amorphous material is sputtered on a metal-coated carrier, our Bulk ONE technology employs high quality, single crystal resonator films, which are used as the enabler to create high performance bulk acoustic wave (BAW) filters. This single crystal material is a key differentiator when compared to the incumbent amorphous thin-film technologies, because it increases the acoustic velocity and the electromechanical coupling coefficient in the resonator, which results in higher filter efficiencies and lower power consumption – which leads to simplified RF front-ends, longer battery life and reduced tissue heating. Our investment during our last fiscal year totaled $0.24M and was focused on single crystal material development and resonator demonstration. Current R&D investments include single crystal materials advancement, technology transfer to our manufacturing partner and resonator development and filter design.

Intellectual Property

We rely on a combination of intellectual property rights, including patents, know-how and trade secrets, along with copyrights, trademarks and contractual obligations and restrictions to protect our core technology and business.

We currently have seven pending patent applications in the United States and intend to file for protection internationally. The patent applications tie directly to our single-crystal bulk acoustic wave (BAW) technology, including materials and device designs, methods of manufacture, integrated circuit designs, wafer packaging, and point of use (to include mobile applications). The Company will continue to innovate and expand our patent portfolio, and when appropriate, we will look to purchase license(s) that grant access to additional intellectual property that enables, enhances or further expands our technical capabilities and/or product offerings.

We believe that it is likely that Akoustis will have competitive advantages from rights granted under our patent applications. Such applications, however, may not result in the issuance of any patents. In addition, any future patent may be opposed, contested, circumvented or designed around by a third party or found to be unenforceable or invalidated. Others may develop technologies that are similar or superior to our proprietary technologies, duplicate our proprietary technologies or design around patents owned or licensed by us.

We generally control access to, and use of, our confidential information through the use of internal and external controls, including contractual protections with employees, contractors and customers. We rely in part on the United States and international copyright laws to protect our intellectual property. All employees and consultants are required to execute confidentiality agreements in connection with their employment and consulting relationships with us. We also require them to agree to disclose and assign to us all inventions conceived or made in connection with the employment or consulting relationship.

Despite our efforts to protect our intellectual property, unauthorized parties may still copy or otherwise obtain and use our software, technology or other information that we regard as confidential and proprietary. In addition, we intend to expand our international presence, and effective patent, copyright, trademark and trade secret protection may not be available or may be limited in foreign countries.

| 17 |

The semiconductor industry is characterized by vigorous protection and pursuit of intellectual property rights and positions, which has resulted in protracted and expensive litigation for many companies. Although we have not received any third party claims, we expect that in the future we may receive communications from various industry participants alleging our infringement of their patents or other intellectual property rights. Any lawsuits could subject us to significant liability for damages, invalidate our proprietary rights and harm our business and our ability to compete. Any litigation, regardless of success or merit, could cause us to incur substantial expenses, reduce our sales and divert the efforts of our technical and management personnel. In the event we receive an adverse result in any litigation, we could be required to pay substantial damages, seek licenses from third parties, which may not be available on reasonable terms or at all, cease the sale of products, expend significant resources to develop alternative technology or discontinue the use of processes requiring the relevant technology.

AkoustisTM and Bulk ONETM are trademarks of Akoustis, Inc.

Competition

The competitive landscape for the Company is small and is controlled by handful of RF component suppliers. These companies include, among others, Avago Technologies Limited, Murata Manufacturing Co., Ltd., Qorvo, Inc., Skyworks Solutions Inc., Taiyo Yuden, and TDK Epcos. Two of these companies dominate the high band filter market, controlling a significant portion of the customer base and are increasing capacity to meet the growth demands of the 4G/LTE market.

We will compete directly with them to secure design slots inside RF front-end modules – targeting companies that procure filters or have captive sources. We believe that our filter designs will be superior in performance and will approach perspective customers as pure-play filter supplier – offering advantages in performance, over the full frequency range, with competitive costs. Our challenge will be to convince the companies that we have a strong intellectual property position, that we will be able to ramp in volume, that we will meet their price targets, and that we can satisfy reliability requirements.

Employees

We have put a premium on hiring the best talent at the right time to enable our core technology and business growth. This includes establishing a competitive compensation and benefits package – enhancing our ability to recruit experienced personnel and key technologists. We currently have 10 full-time employees plus 10 independent contractors working with the Company, and we will continue to hire specific and targeted positions to further enable our technology and manufacturing capabilities.

Properties

Our headquarters in Huntersville, NC, is a 4,800 square foot facility that we lease for $4,596 per month, with a term expiring in April 2018. We believe that our facilities are sufficient to meet our current needs, and we will look for suitable expansion as and when needed.

| 18 |

An investment in OUR securities is highly speculative and involves a high degree of risk. We face a variety of risks that may affect our operations or financial results and many of those risks are driven by factors that we cannot control or predict. Before investing in the securities you should carefully consider the following risks, together with the financial and other information contained in this report. If any of the following risks actually occurs, our business, prospects, financial condition and results of operations could be materially adversely affected. In that case, the trading price of our common stock would likely decline and you may lose all or a part of your investment. Only those investors who can bear the risk of loss of their entire investment should consider an investment in our securities.

THIS REPORT CONTAINS CERTAIN STATEMENTS RELATING TO FUTURE EVENTS OR THE FUTURE FINANCIAL PERFORMANCE OF OUR COMPANY. PROSPECTIVE INVESTORS ARE CAUTIONED THAT SUCH STATEMENTS ARE ONLY PREDICTIONS AND INVOLVE RISKS AND UNCERTAINTIES, AND THAT ACTUAL EVENTS OR RESULTS MAY DIFFER MATERIALLY. IN EVALUATING SUCH STATEMENTS, PROSPECTIVE INVESTORS SHOULD SPECIFICALLY CONSIDER THE VARIOUS FACTORS IDENTIFIED IN THIS REPORT, INCLUDING THE MATTERS SET FORTH BELOW, WHICH COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE INDICATED BY SUCH FORWARD-LOOKING STATEMENTS.

If any of the following or other risks materialize, the Company’s business, financial condition, and results of operations could be materially adversely affected which, in turn, could adversely impact the value of our Common Stock. In such a case, investors in our Common Stock could lose all or part of their investment.

Prospective investors should consider carefully whether an investment in the Company is suitable for them in light of the information contained in this Report and the financial resources available to them. The risks described below do not purport to be all the risks to which the Company or the Company could be exposed. This section is a summary of certain risks and is not set out in any particular order of priority. They are the risks that we presently believe are material to the operations of the Company. Additional risks of which we are not presently aware or which we presently deem immaterial may also impair the Company’s business, financial condition or results of operations.

Risks Related to our Business and the Industry in Which We Operate

We have a limited operating history upon which investors can evaluate our business and future prospects.

We are an early stage company that has not yet begun any commercial operations. Historically, we have been a shell company with no operating history and no assets other than cash. Upon consummation of the Merger with Akoustis, we redirected our business focus towards the development of advanced single crystal bulk acoustic wave filter products for RF front-ends for use in mobile wireless device industry. Although Akoustis since its inception focused its activity on research and development (“R&D”) of high efficiency acoustic wave resonator technology utilizing single crystal piezoelectric materials, this technology has not yet obtained marketing approval or been verified in commercial manufacturing, and its RF filters have not generated any sales.

| 19 |

Since our potential customers and future demand for our products are based on estimates of planned operations rather than experience, it is difficult for our management and our investors to accurately forecast and evaluate our future prospects and our revenues. Our proposed operations are therefore subject to all of the risks inherent in light of the expenses, difficulties, complications and delays frequently encountered in connection with the formation of any new business, the development of a product, as well as those risks that are specific to our business in particular. An investment in an early stage company such as ours involves a degree of risk, including the possibility that entire investment may be lost. The risks include, but are not limited to, the possibility that following the Merger, we will not be able to develop functional and scalable products, or that although functional and scalable, our products and/or services will not be accepted in the market. To successfully introduce and market our products at a profit, we must establish brand name recognition and competitive advantages for our products. There are no assurances that the Company can successfully address these challenges. If it is unsuccessful, the Company and its business, financial condition and operating results will be materially and adversely affected.

We may not generate revenues or achieve profitability.

We have incurred operating losses since our inception and expect to continue to have negative cash flow from operations. We have never generated any revenues; our only income has been from R&D grants. We experienced net losses of approximately $0.44 million for the period from May 12, 2014 (inception) to March 31, 2015. We have accumulated losses to date of approximately $0.5 million. Our future profitability will depend on our ability to create a sustainable business model and generate revenues, which is subject to a number of factors, including our ability to successfully implement our strategies and execute our R&D plan, our ability to implement our improved design and cost reductions into manufacturing of our RF filters, the availability of funding, market acceptance of our products, consumer demand for end products incorporating our products, our ability to compete effectively in a crowded field, our ability to respond effectively to technological advances by timely introducing our new technologies and products and global economic and political conditions.

Our future profitability also depends on our expense levels, which are influenced by a number of factors, including the resources we devote to developing and supporting our projects and potential products, the continued progress of our research and development of potential products, our ability to improve research and development efficiencies, license fees or royalties we may be required to pay, and the potential need to acquire licenses to new technology, the availability of intellectual property for licensing or acquisition, or to use our technology in new markets, which could require us to pay unanticipated license fees and royalties in connection with these licenses.

Our development and commercialization efforts may prove more expensive than we currently anticipate, and we may not succeed in increasing our revenues to offset higher expenses. These expenses, among other things, may cause our net income and working capital to decrease. If we fail to generate revenue and manage our expenses, we may never achieve profitability, which would adversely and materially affect our ability to provide a return to our investors

The industry and the markets in which the Company operates are highly competitive and subject to rapid technological change.

The markets in which we intend to compete are intensely competitive. We will operate primarily in the industry that designs and produces semiconductor components for wireless communications and other wireless devices, which is subject to rapid changes in both product and process technologies based on demand and evolving industry standards. The intended markets for our products are characterized by:

| · | rapid technological developments and product evolution, |

| 20 |

| · | rapid changes in customer requirements, |

| · | frequent new product introductions and enhancements, |

| · | continuous demand for higher levels of integration, decreased size and decreased power consumption, |

| · | short product life cycles with declining prices over the life cycle of the product, and |

| · | evolving industry standards. |

The continuous evolutions of these technologies and frequent introduction of new products and enhancements have generally resulted in short product life cycles for wireless semiconductor products, in general, and for RF front-end products, in particular. Our products could become obsolete or less competitive sooner than anticipated because of a faster than anticipated change in one or more of the above-noted factors. Therefore, in order for our RF filters to be competitive and achieve market acceptance, we need to keep pace with rapid development of new process technologies, which requires us to:

| · | respond effectively to technological advances by timely introducing our new technologies and products, |

| · | successfully implement our strategies and execute our R&D plan in practice, |

| · | improve the efficiency of our technology, |

| · | implement our improved design and cost reductions into manufacturing of our RF filters. |

Our products may not be accepted in the market.

Although we believe that our Bulk ONE acoustic wave resonator technology that utilizes single crystal piezoelectric materials will provide material advantages over existing RF filters and are currently developing various methods of integration suitable for implementation of this technology to RF filters, we cannot be certain that our RF filters will be able to achieve or maintain market acceptance. While we have fabricated R&D resonators that demonstrate the feasibility of our Bulk ONE technology, we are still in the process of transitioning this technology into a production-capable wafer fabrication facility for manufacturing of our RF filters, and this technology is not verified yet in practice or on a commercial scale. There are also no records that can demonstrate our ability to successfully overcome many of the risks and uncertainties frequently encountered by companies in new and rapidly evolving fields. In addition to our limited operating history, we will depend on a limited number of manufacturers and customers for a significant portion of our revenue in the future. Each of these factors may adversely affect our ability to implement our business strategy and achieve our business goals.

The successful development of our Bulk ONE technology following the Merger and market acceptance of our RF filters will be highly complex and will depend on the following principal competitive factors, including our ability to:

| · | comply with industry standards and effectively compete against current technology for producing RF acoustic wave filters, |

| · | differentiate our products from offerings of our competitors by delivering RF filters that are higher in quality, reliability and technical performance, |

| 21 |

| · | anticipate customer and market requirements, changes in technology and industry standards and timely develop improved technologies that meet high levels of satisfaction of our potential customers, |

| · | maintain, grow and manage our internal teams to the extent we increase our operations and develop new segments of our business, |

| · | develop and maintain successful collaboration, strategic, and other relationships with our manufacturers, customers and contractors, |

| · | protect, develop or otherwise obtain adequate intellectual property for our technology and our filters; and |

| · | obtain strong financial, sales, marketing, technical and other resources necessary to develop, test, manufacture, commercialize and market our filters. |

If we are unsuccessful in accomplishing these objectives, we may not be able to compete successfully against current and potential competitors. As a result, our Bulk ONE technology and our RF filters may not be accepted in the market and we may never attain profitability.

We will face intense competition, which may cause pricing pressures, decreased gross margins and loss of market share and may materially and adversely affect our business, financial condition and results of operations.

We will compete with U.S. and international semiconductor manufacturers and fabless mobile semiconductor companies of all sizes in terms of resources and market share, some of whom have significantly greater financial, technical, manufacturing and marketing resources than we do. We expect competition in our markets to intensify, as new competitors enter the RF component market, existing competitors merge or form alliances, and new technologies emerge. Our competitors may introduce new solutions and technologies that are superior to our BAW technology, are verified on a commercial scale, and have achieved widespread market acceptance. Certain of our competitors may be able to adapt more quickly than we can to new or emerging technologies and changes in customer requirements or may be able to devote greater resources to the development, promotion and sale of their products than we can. This implementation may require us to modify the manufacturing process for our filters, design new products to more stringent standards, and redesign some existing products, which may prove difficult for us and result in delays in product deliveries and increased expenses.

Increased competition could also result in pricing pressures, declining average selling prices for our RF filters, decreased gross margins and loss of market share. We will need to make substantial investments to develop these enhancements and technologies, and we cannot assure investors that we will have funds available for these investments or that these enhancements and technologies will be successful. If a competing technology emerges that is, or is perceived to be, superior to our existing technology and we are unable to adapt to these changes and to compete effectively, our market share and financial condition could be materially and adversely affected, and our business, revenue, and results of operations could be harmed.

Changes in general economic conditions, together with other factors, cause significant upturns and downturns in the industry, and our business, therefore, may also experience cyclical fluctuations in the future.

From time to time, changes in general economic conditions, together with other factors, may cause significant upturns and downturns in the semiconductor industry. These fluctuations are due to a number of factors, many of which are beyond our control:

| 22 |

| · | levels of inventory in our end markets, |

| · | availability and cost of supply for manufacturing of our RF filters using our design, |

| · | changes in end-user demand for the products manufactured with our technology and sold by our customers, |

| · | industry production capacity levels and fluctuations in industry manufacturing yields, |

| · | market acceptance of our customers’ products that incorporate our RF filters, |

| · | the gain or loss of significant customers, |

| · | the effects of competitive pricing pressures, including decreases in average selling prices of our RF filters, |

| · | new product and technology introductions by competitors, |

| · | changes in the mix of products produced and sold, and |

| · | intellectual property disputes. |

As a result, the demand for our products can change quickly and in ways we may not anticipate, and our business, therefore, may also experience cyclical fluctuations in the future operating results. In addition, future downturns in the electronic systems industry could adversely impact our revenue and harm our business, financial condition and results of operations.

If we are unable to attract and retain qualified personnel to contribute to the development, manufacture and sale of our products, we may not be able to effectively operate our business.

As the source of our technological and product innovations, our key technical personnel represent a significant asset. We believe that our future success is highly dependent on the continued services of our current key officers, employees, and Board members, as well as our ability to attract and retain highly skilled and experienced technical personnel. The loss of their services could have a detrimental effect on our operations. Specifically, the loss of the services of Jeffrey Shealy, our President and CEO, Prof. Steve Denbaars, our director, Mark Boomgarden, our Vice President of Operations, David Aichele, our Vice President of Business Development, Prof. James Shealy, the Chair of our Scientific Advisor Board, Cindy Payne, our Chief Financial Officer, Richard Ogawa, our Patent Counsel, any major change in our Board or management, or our inability to attract, retain and motivate qualified personnel could have a material adverse effect on our ability to operate our business. The competition for management and technical personnel is intense in the wireless semiconductor industry, and therefore we cannot assure you that we will be able to attract and retain qualified management and other personnel necessary for the design, development, manufacture and sale of our products.

| 23 |

We expect to substantially rely on third parties to manufacture our RF filters.

We employ a “fabless” business strategy, meaning that we do not own a semiconductor fabrication facility, or fab, and do not currently have, nor do we plan to acquire, the infrastructure or capability internally, such as our own manufacturing facilities, to manufacture our wafers and our filters for use in the conduct of commercial quantities. Instead, we leverage capital investments and capacity of manufacturers to fabricate our wafers. Therefore, success of implementation of our single-crystal BAW technology for manufacturing our RF filters and its commercial production will substantially depend upon our ability to develop, maintain and expand our strategic relationships with manufacturers that will fabricate wafers using our design and incorporate them into their products. Any impairment in our relationship with these manufacturers could have a material adverse effect on our business, results of operations, cash flow and financial condition. Although we have entered into a joint development agreement and a foundry agreement with Global Communication Semiconductors, LLC (“GCS”), and may explore other plans to enter into agreements with more manufacturers, to fabricate our RF filters for R&D and for commercial sales, there can be no assurance that we will be able to retain those relationships on commercially reasonable terms, if at all. Since we expect to depend upon one or a limited number of these manufacturers for a signification portion of our revenue in the future, we could experience delays in the launch and commercial productions of our RF filters if we are unable to maintain those relationships.

Reliance on a limited number of manufacturers also may expose us to the following risks:

| · | We may be unable to identify manufacturers on acceptable terms, or at all, because the number of potential manufacturers is limited. In addition, a new manufacturer would have to be educated in, or develop substantially equivalent processes for manufacturing of our wafers. |

| · | Our manufacturers might be unable to formulate and manufacture wafers in the volume and of the quality required to meet demands of our R&D and commercial needs. |

| · | Our future manufacturers may not perform as contractually agreed or may not remain in the manufacturing business for the time required to successfully produce, store and distribute our products. |

| · | Since our filters are not sold directly to the end-user, but are components of other products, we highly depend upon selection of our design and technology by these manufacturers from among alternative offerings and including and incorporating our filters into their final product. |

Each of these risks could delay the commercialization of our RF filters and its market acceptance or result in higher costs or deprive us of potential product revenues.

We rely on our independent contractors in adequately performing their contractual obligations, meeting expected deadlines and applicable regulatory requirements